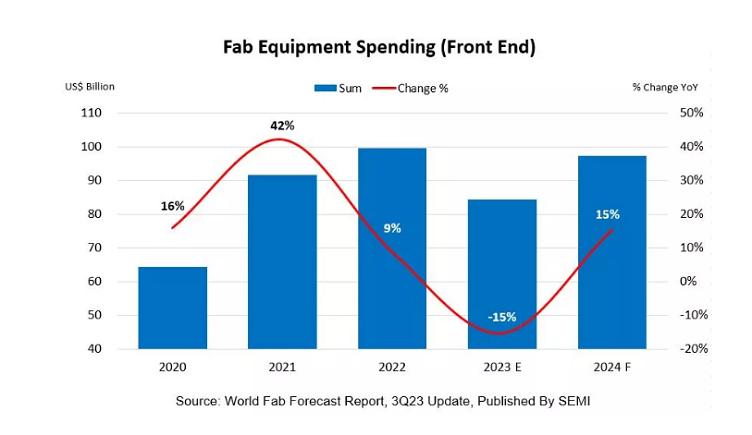

Due to softening chip demand and elevated inventory, semiconductor fab equipment spending this year is expected to decline 15% year-over-year. The good news is that a bounce back is expected in 2024, according to new research from SEMI.

The organizational body said front-end facility spending on equipment will rebound by 15% to $97 billion in 2024. In 2023, front-end facility spending is forecast to be $84 billion, down from a record in 2022 of $99.5 billion.

The recovery in 2024 will come from the end of the semiconductor inventory correction and the strengthening of demand in the high-performance computing and memory segments, SEMI said.

“The 2023 decline in equipment investment is proving shallower and the 2024 rebound stronger than expected earlier this year,” said Ajit Manocha, SEMI president and CEO. “The trend suggests the semiconductor industry is turning the corner on the downturn and on a path back to robust growth fueled by healthy chip demand.”

Taiwan is expected to retain the global lead in fab equipment spending in 2024 with $23 billion in investments. Korea will rank second in spending with about $22 billion in investments. China will likely be third in 2024 at $20 billion. This will be a decline from 2023 due to Chinese foundry suppliers expecting to continue to invest in mature process nodes.

America will remain in the fourth largest region in equipment spending but will reach a new high of $14 billion in investments in 2024, a 23% year-over-year increase, SEMI forecasts. The Europe and Middle East sector will also log record investments next year.