Globalization of the electronics supply chain helped kick off a huge migration of manufacturing capacity to Southeast Asia. Today, it’s fair to say that “most” of the manufacturing capacity for electronic components and assemblies has been offshored from consumer markets. One factor that aided this transition to a global supply chain was low logistics and shipping costs, particularly from China. Semiconductor component costs have also come down significantly over the past 30 years in accordance with scaling laws.

Over the past 20 years, that tide has slowly turned as logistics costs have generally risen, and there has been significant volatility in component costs driven by shortages and broker activity. The most obvious recent event where this occurred was during the COVID-19 crisis and subsequent increase of consumer demand driven by stimulus in industrialized countries. The unprecedented demand coupled with a labor shortage and general parts/raw materials shortage shows up in pricing for shipping, electronic components, and ultimately inflation for producer and consumer goods.

Which costs are most affected?

What effect do these factors play in driving the costs of electronics manufacturing? Generally, three areas should be examined:

- Logistics and sourcing costs

- Parts and production costs

- Intangible costs

Let’s look at each of these three cost drivers in today’s production and sourcing environment.

Low volume versus high volume production

The differences in costs for parts become very clear when high-volume and low-volume production are compared. There is a general cost issue that affects everyone, and then there are volume-specific sourcing issues that arise due to the ability to receive allocation from semiconductor manufacturers.

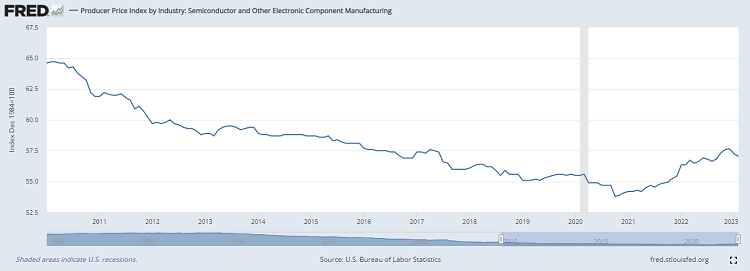

Over the long march of time since the mid-1990s, the costs to produce components have decreased while semiconductor manufacturer margins have remained relatively constant. According to Federal Reserve Economic Data (FRED), producer pricing in the electronic components and semiconductor sector saw the largest increase since October 2020, reaching a 7% increase in component costs charged to wholesale customers and distributors.

Electronic manufacturing costs over the past 20 years. Source: FRED

Electronic manufacturing costs over the past 20 years. Source: FRED

For low-volume production, the situation is much worse as companies have been more often forced to rely on broker networks. Smaller producers and OEMs might not be able to get allocation from semiconductor manufacturers, so they must go use distributors and a network of brokers to obtain components.

Overseas brokers have been ruthless in buying up stocks of popular components from western distributors and reselling these parts at huge markups. This creates risks of theft, fake components, defective real components, and extreme costs for all of the above. The risk-reward profile is unacceptable for many companies, so they may simply opt to not produce or repeatedly modify designs to accommodate substitute parts. It is then more difficult to work with a fab and assembly vendor as they will not always offer the same level of volume pricing when accommodating variants. Ultimately, these part costs get passed to the end customer.

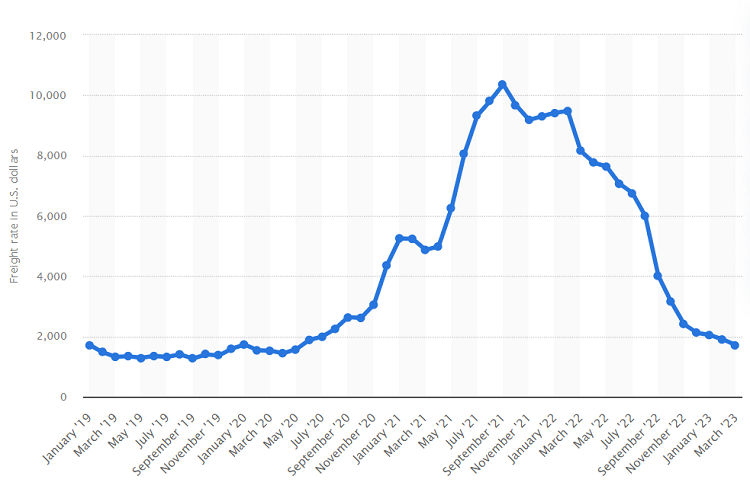

Freight container costs jumped substantially during the last few years before settling back down, showing how vendors need to factor this into costs. Source: Statista

Freight container costs jumped substantially during the last few years before settling back down, showing how vendors need to factor this into costs. Source: Statista

Container costs return to normal in 2023

Following the 2020-2021 explosion of consumer demand, then the later tightening of monetary policy and credit, the freight rate has essentially returned to normal as consumer demand for products manufactured overseas declines.

Other data from Bloomberg’s Freightos Global Container Index shows similar astronomical rises in the freight rate for container shipping. According to IMF data, shipping costs alone accounted for up to 5% reduction in margin (on a dollar basis) for many businesses. Companies then have to make the difficult decision of how to balance those additional costs through expense reduction, price increases, change in sourcing model, or a combination of these strategies. Shipping costs alone were then projected to account for 1.5% of worldwide price inflation.

Intangible costs

There are additional costs that are not obvious simply by looking at parts and shipping costs. These cannot always be passed to the end customer, but they do impact a company’s ability to be competitive and gain a first-mover advantage over other businesses in the same industry/vertical. Some of the intangible factors that affect electronic manufacturing costs include:

- Impaired competitiveness due to component delivery delays or out-of-stock parts.

- Increased design effort due to variant creation.

- Lost market share due to product delivery delays.

Intangible costs are hard to quantify and are not obvious until they have already been incurred, so it is difficult to pass these onto a customer. Instead, companies have to address these problems operationally in the hopes that they can maintain a sustainable supply of raw materials and parts, stay on production schedules, and ultimately deliver product to market.

Summary

The costs outlined in this article will always persist in the electronics industry. Recent events on the world stage have made control over these costs much more important, and they have hit closer to home for consumers who just want to purchase the latest gadgets.

To summarize, some courses of action designers can take for cost control include:

- Identify possible alternative components and regulatory constraints early.

- Create orders early and lock-in part selections based on features.

- To help balance parts availability with demand, create design variants before production.

Design teams need to anticipate problems, not react to them. The challenges outlined above are waning for now, but we all know the cyclical nature of electronics production and consumer demand. Some additional planning on the front end can keep companies competitive and on-schedule on the back end, and some prototyping spins might be eliminated as well.