Smart grid deployment is proceeding in fits and starts around the world. Europe and North America are leading the way, embracing first-mover risks and rewards. China, with its deep pockets, is biding its time, building out a grid with some embedded intelligence. Meanwhile, India must deal with significant energy-generation problems before tackling grid modernization.

Each region has its own set of issues, and there are plenty of regulatory and technical pitfalls for OEMs in each region. Even so, growth is expected to be steady to strong for deploying key elements of a power grid designed to increase reliability and reduce outages while reintroducing energy efficiency as a key component of national energy strategies in the 21st century.

In North America, the emphasis is on improving grid reliability while weighing trade-offs between retrofits and costly upfront investments, versus European planners focused on looming emission and efficiency deadlines and also looking to integrate renewable energy sources into their evolving, two-way power transmission networks. And China, which is in a position to learn from the mistakes of others, could end up leapfrogging the field by replacing a relatively antiquated power distribution system with a state-of-the-art smart grid.

In all regions, the smart grid promises to improve reliability, promote energy efficiency, reduce ratepayer costs and provide a return on substantial government R&D and industry capital investments. The catchall phrase “smart grid” refers to a range of tools and technologies being integrated to modernize often aging electric grids. Not only will smart grids support the two-way flow of electricity and information between utilities and consumers, they will also integrate diagnostic tools to monitor grid condition and help manage demand response and outages.

In the Anthropocene, the emerging epoch in which human activities influence the Earth’s ecosystems, the smart grid also will be more resilient as extreme weather events are projected to grow in frequency.

“The big thing the smart grid can do is make it easier to manage the grid and to restore power faster after a blackout,” said Alison Silverstein, who manages a U.S. effort to use analytical tools for grid management as a way to improve reliability. The effort, called the North American SynchroPhaser Initiative (NASPI), employs monitoring devices called phasor measurement units (PMUs) to determine, as Silverstein described it, “the true condition of the grid.”

PMUs typically collect 30 observations a second. This real-time data can be leveraged to improve the ability of utilities to diagnose problems and come up with options for restoring power.

In other words, Silverstein said, smart grids will have the capability to provide a kind of situational awareness along with intelligence in the form of two-way communications and other electronics functionality.

R&D “pulls” industry investment

U.S.-funded programs like NASPI and other long-term R&D efforts to improve power grid reliability have also had another impact, Silverstein said. The investments have created an “industry pull” that has translated into greater investment in grid technologies, such as synchrophaser measurement.

As of March 31, the U.S. Department of Energy (DOE) estimates that the government's smart grid initiative has attracted total investments of nearly $3.6 billion in advanced metering equipment, more than $1.1 billion for distribution equipment and $360 million for transmission infrastructure.

The investment landscape has also been improved by the fact that industry standards for diagnostic tools like PMUs were "locked down" several years ago, Silverstein said. The result is that synchrophaser monitoring tools are now being added to grid infrastructures around the world.

NASPI is funded by DoE and the North American Electric Reliability Corp. Industry volunteers provide much of the brainpower. Other U.S. efforts have focused on spurring investment in smart grid deployment by seeding the market for grid modernization with U.S. economic stimulus funding.

As of June, the DoE estimates that more than 15 million smart meters, associated hardware and networks have been deployed in the U.S. under its grant program at a total cost of $3.26 billion. Roughly half of that deployment has been funded through the 2009 American Recovery and Reinvestment Act. The legislation provided $4.5 billion in federal funding that was matched by an additional $4.5 million private sector investment.

DoE and commercial builders recently challenged manufacturers of grid components to come up with a wireless sub-meter that costs less than $100. Sub-metering gives building managers information on energy usage they can leverage to improve energy efficiency. DoE said its industry partners have agreed to buy the low-cost wireless sub-meters if and when they hit the market.

Optimizing power flow

Utilities and power authorities are also beginning in earnest to deploy key components and applications as they build out the smart electricity grid in North America, Europe and Asia. Among them are volt/VAR optimization (VVO) devices used to optimize power flow across the grid. Global shipments of VVO control electronics are forecast to double during the next five years to 100,000 units, according to IHS.

The intelligence embedded in grid electronics in the form of dedicated VVO software is also expected to proliferate as smart grid networks are built out. Estimates of annual revenues for VVO software quadrupling by 2018 have already prompted some OEMs to acquire grid software and analytics firms. For example, Swiss energy giant ABB acquired Atlanta-based software specialist Ventyx for more than $1 billion.

Other acquisitions, like Siemens' 2012 deal to buy Canadian network supplier RuggedCom, also signal increased interest by European firms to gain a foothold in the North American smart grid market, where margins for suppliers will likely be higher than, say, China.

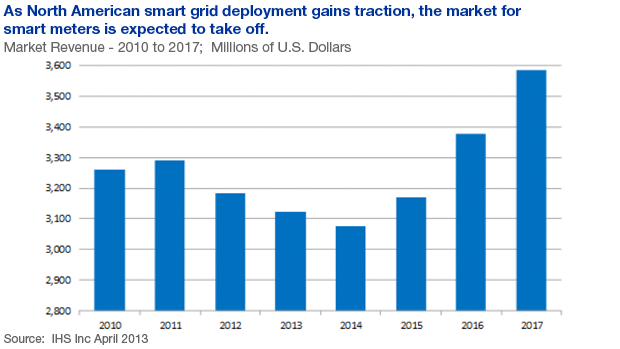

IHS forecasts that the North American market for distribution automation and grid networking gear will grow to $1.7 billion annually.

Through 2016, meanwhile, global shipments of basic electricity meters are expected to drop by half worldwide to an estimated 60 million units. Shipments of advanced meters, defined as any type with embedded communications that allow the meter to be read remotely, are expected to reach 90 million by 2016. IHS expects the installed base of advanced meters to top 600 million end points by 2016, or about 40 percent of the installed base.

Electricity meters are widely seen as the starting point for grid modernization. Hence, they need to be interoperable, or “future proof” — that is, adaptable to the evolving requirements of power utilities and grid operators.

The future proofing of smart grid components like advanced meters refers to the requirement for design equipment to adapt to new technologies while continuing to operate with legacy apparatus. Therefore, these components must be designed to allow for upgrades at very little additional cost.

In developed countries, adoption of home area networks is also seen as important for the growth of the global electricity meter market. High-end applications include interfaces to consumer electronics, energy management with distributed end-use loads, energy storage and distributed generation.

The emerging smart grid market will require agile suppliers. What follows is a regional look at the current state of smart grid deployment:

China plays leapfrog

Observers estimate that nearly three-quarters of all installed electricity meters in China will include communications.

For now, most of what is being shipped to China is "advanced" one-way meters equipped with RS485 ports being installed in apartment buildings that are sprouting like weeds in Chinese cities. While some two-way meters with smart grid functionality are being shipped to China, IHS reckons that advanced one-way meters will predominate in the interim to facilitate meter reading in apartments that use relatively little electricity because they lack air conditioning.

In the long term, China will “adopt technologies and learn from our mistakes,” said Jacob Pereira, an IHS utility infrastructure analyst based in Austin, Texas. He expects China’s giant state-run power utility to continue its focus on getting the lights turned on across China. As that effort gains momentum, China could eventually leapfrog other regions by replacing a relatively backward power distribution system with a state-of-the-art smart grid. That will be made easier because the conversion is being overseen by a single, state-run utility. By contrast, the roughly 3,500 U.S. utilities are regulated at the state level.

China is making great strides in power generation as its leaders come to the realization that burning high-sulfur coal to generate electricity is unsustainable. The nation’s dominance in the solar power industry is well-documented, but it also leads the world in wind power. Indeed, China's grid-linked wind capacity is expected to reach 100 gigawatts by 2015, according to a World Bank survey.

Europe

One likely outcome of smart grid deployment could be greater decentralization of power distribution, especially in the U.S. and Europe. The current system relies heavily on large coal-fired or nuclear power plants generating electricity that must be delivered over long transmission lines. These centralized systems waste large amounts of power in transmission.

In places like Germany, which has embarked on a so-called "energy turnaround," some industrial power users are building their own generating capacity. In some cases, that's being done to avoid surcharges on the use of renewable energy. Either way, the new generating capacity will have to be integrated into Germany's expanding power grid.

Smart grids promise to change the distribution model. Power distribution based on smart grid technology "will be more localized," Pereira agreed.

Europe is, in many ways, furthest down the road to smart grid deployment. Driving much of this power surge is an ambitious set of targets established by the European Union in 2007 called "20-20-20." The binding legislation seeks to reduce EU greenhouse gases, increase renewable energy sources and boost EU energy efficiency — all three by 20 percent. The goals must be reached by 2020.

With that in mind, European regulators launched a standards effort for "smart metering" (water, gas, electricity and heating) in 2009. The goal is to ensure interoperability of utility meters as part of the larger 20-20-20 initiative. A separate smart grid standards effort followed in 2011 to develop a framework for integrating embedded electronics and communications into smart grid devices along with network security and privacy features.

The goal, according to Siemens executive Ralph Sporer, who heads the European Commission's smart grid coordination group, is "a set of consistent standards, which will support the information exchange [like] communication protocols and data models and the integration of all users into the electric system operation."

The EU's ambitious energy goals mean utilities will be buying large quantities of two-way smart meters in order to meet the 20-20-20 mandate. As a result, IMS is forecasting that the average price of two-way meters will contract 25 percent by 2016.

Setting the pace for European smart grid deployment is Germany, which has decided to shutter its nuclear power plants by 2022. Meantime, it is constructing a "power highway" consisting of a transmission network designed to move electricity generated by solar installations and wind farms in the northern part of the country to manufacturing centers in the south. Also by 2022, 48 percent of Germany's power will be generated by renewable sources.

All this will require construction of 4,000 kilometers (about 2,500 miles) of new transmission lines by 2022 as part of Germany's "energy turnaround" initiative away from nuclear power and toward renewables. Underpinning the German energy pivot is a transmission network known as the Grid Development Plan.

"What we need now is better coordination among the renewables expansion, the network expansion and system integration," explained Stephan Kohler, chief executive of the German Energy Agency, a research group. "We must draw up regional development plans for the renewables and bring them together in a comprehensive nationwide concept to ensure that overcapacities are avoided and that our resources and money are not wasted."

The agency estimated that Germany's Grid Development Plan could potentially add 220 gigawatts of power plant capacity by 2022. However, much system integration work will be needed to accommodate an estimated 54 gigawatts for photovoltaic and 48 gigawatts for wind turbine capacity, the group noted.

The good news, so far, is that large amounts of renewable energy are being generated — at least when the sun is shining and wind blowing — and has been given priority access on the power grid. The bad news is that Germany's grid expansion projects are reportedly behind schedule. This is compounded by the fact that energy storage technology development is lagging behind renewable power generation and smart grid efforts.

One result, economists argue, is energy price distortions when, for example, excess power generated in Germany is pushed to the European grid at a loss — sometimes referred to as "unscheduled power flows."

Pereira added that the EU's smart grid push faces "very expensive — and often not fiscally viable — equipment installations [that] are unlikely to be popular in a place where the average electricity prices are already four times what they are in the U.S."

The German energy group argues that the shift away from nuclear and coal to solar and wind power underscores the need for smart grid deployment. "Renewable energy sources cannot be efficiently integrated unless the grids are both expanded and made subject to intelligent control," it stressed earlier this year in calling for "rectification" of Germany's energy conversion.

Critics warn that European policy makers will have to come up with realistic assessments of how the 20-20-20 targets can be met, how much it will cost and how downstream risks can be mitigated.

North America

Across the Atlantic, where a boom in shale exploration has driven down natural gas and electricity prices, much of the focus has been on leveraging smart grid technologies to improve grid reliability. The reliability push also includes upgrading components like reclosers used to isolate faults such as short circuits when a falling tree branch snaps a power transmission line or blows a transformer. Reclosers are used to isolate outages by dividing the grid into smaller sections to limit blackouts. Such capabilities are growing in importance as extreme weather events undermine the reliability of the current electrical grid.

Pereira and other observers suspect that the high cost of transmission components will limit upfront investments in smart grid technologies by U.S. utilities. One reason is that those costs would have to be justified in order to convince regulators to approve rate increases.

Investments in new transmission equipment will be expensive, and the return on that investment will take time. In many cases, it's cheaper to simply wait for components to fail, and then retrofit.

Meanwhile, work on standardizing North American smart grid components like meters and synchrophasers is well underway, signaling that technology is maturing and that the pace of deployment is quickening. For example, the IEEE said it has either approved or is developing more than 100 smart grid standards covering aspects ranging from interoperability of electric power to specifications for integrating renewable energy into the grid.

India

According to a 2010 World Bank report, one-third of India's 1.24 billion inhabitants lack access to reliable electricity. Adding to India's energy woes is its continuing heavy reliance on coal, which accounts for about 55 percent of its generation capacity.

Because of this, the government has launched a "power to all" initiative that, among other things, seeks to attract foreign direct investment in India's energy sector, including grid reliability and security. India has, so far, approved outside investments totaling more than $1 billion in grid equipment and automation tools.

In energy markets like India, where power outages are a way of life, electricity theft remains a problem. Pereira said smart metering could help utilities address the problem. Dedicated micro-grids are another option, along with intermediate applications like improved distribution monitoring and metering.

“India will certainly need to continue to invest in its utility infrastructure to support growth and prevent massive blackouts and brownouts,” Pereira said, but “political paralysis” remains a reality.

Given the varying smart grid requirements and challenges in each market, it's difficult to gauge which region will be most promising for suppliers. All things considered, Pereira concludes that “China represents the biggest opportunity for OEMs, especially for component manufacturers, such as those who design and manufacture semiconductors.”

But it won't be easy for outside technology manufacturers to penetrate a Chinese electricity sector tightly controlled by a state grid corporation. Some OEMs have opted to join with Chinese partners, an arrangement fraught with intellectual property issues.

China's state-run enterprises also tend to go with the lowest-cost vendors to create huge economies of scale, Pereira added, resulting in aggressive pricing. As with many emerging technologies, that will mean very thin margins for future suppliers to China's electricity sector.