Companies are just now starting to get funding from the U.S. CHIPS and Science Act and European Chips Act (ECA). While both regions are expanding their fabrication capacity, these sectors are certainly not the only ones.

However, looking at the statistics on the fabrication capacity being built across the world countries in Southeast Asian are also upping the total wafer fabrication capacity coming online in the next few years.

Wafer capacity vs. number of fabs

There are a few ways to measure how much new foundry capacity will be available in different parts of the world. These metrics can be used for fabrication capacity and output:

- Monthly or annual wafer capacity

- Number of foundry sites being built

- Number of captive sites being built

Foundry capacity and number of foundry sites are two competing metrics which are not comparable. Larger foundries can have higher monthly capacity in a single location, which is being allocated to client companies who may be fabless. Captive capacity is dedicated to a company’s own products, so it is often overlooked in the discussion of foundries and industrial capacity.

First, examine the total monthly wafer capacity being developed by various companies, which is summarized in the table below. These numbers refer to new foundry capacity; the table does not include new captive capacity for a company’s own products.

The entry at the bottom for Semiconductor Manufacturing International Corporation (SMIC) is indicative of the Chinese strategy in semiconductor manufacturing. There is an emphasis on foundry capacity which would be used to produce products from local or foreign companies rather than on developing a homegrown industry with captive manufacturing. It is interesting that this would be the approach given that the U.S. (China’s biggest customer) has focused more on captive capacity rather than foundry.

In terms of the number of facilities, the U.S. was solidly in the lead at the end of 2023. Throughout the U.S., there are 73 new semiconductor fabrication facilities that are planned for construction or are currently under construction, either as expansions of existing facilities or as brand-new facilities. In total, there are 50 brand new facilities being built by U.S. companies, and 42% of those brand-new facilities are in the U.S.

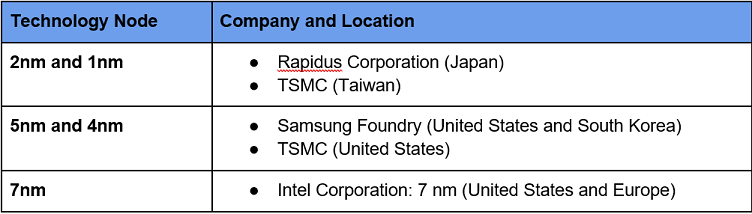

Technology node and location

Not all fabrication facilities or foundry capacity are created equal because not all fabs can produce at the same technology node. When we look at technology node distribution globally, we see some interesting figures that indicate the type of products available in different parts of the world. This is outlined in the table below.

The list above illustrates a few important points about fabrication capacity; Intel is still playing catchup to Samsung and TSMC, despite their intent to leapfrog the latter. The most advanced commercialized capacity is now coming to the U.S. with TSMC and Samsung manufacturing at 5 nm and 4 nm nodes, but the most advanced foundry capacity (2 nm and 1 nm nodes) will remain in Asia for the foreseeable future.

US and EU investment dollars dominate

While it is true that companies in China, most notably SMIC, are bringing significant manufacturing online, the U.S. and EU public investments are the most significant among all the investments listed above. Collectively, the CHIPS and Science Act and European Chips Act have allocated $100 billion to support investment in new fabrication capacity, as well as research and development. That’s not the most important part; the U.S. public investment alone kicked off nearly triple that amount in private investment into the semiconductor industry.

The European Chips Act explicitly states a very simple goal: to double the EU’s semiconductor manufacturing market share over the next decade. The current market share in the EU is 10% and doubling to 20% would require growth of homegrown industrial players like Infineon and STMicroelectronics to expand in the EU, as well as attracting foreign manufacturers to build new plants in Europe.

While U.S. foundry capacity may not be dominant, U.S. companies are still investing huge amounts of money in captive fabrication capacity. Some of the names making the biggest headlines are Intel, Texas Instruments and Micron, all of which are expanding their local capacity in the U.S. Whether these investments return the U.S. to market dominance is questionable given the Chinese foundry capacity increase, but it does improve U.S. independence from Southeast Asia.