Samsung may have lost a battle in the competitive smartphone market last summer when it was hit with more than $1 billion in damages for infringing Apple patents. But by the end of the year, the South Korean electronics giant certainly seemed to be winning the war.

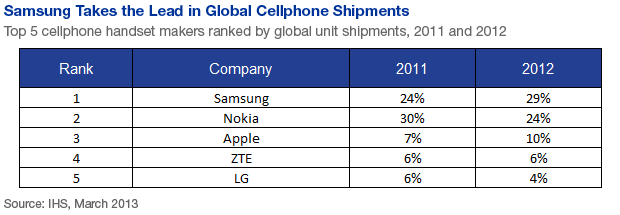

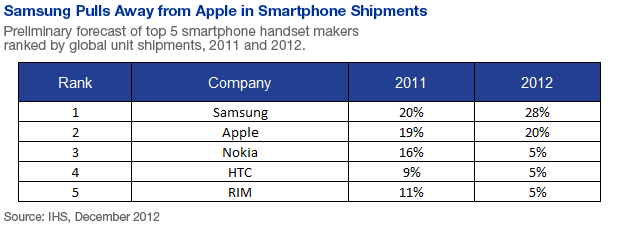

In 2012, Samsung displaced Nokia as the leader in mobile handset shipments globally, shipping 29 percent of all mobile phones compared to 24 percent by Nokia, according to IHS. This year, IHS expects Samsung to extend that lead by 11 percentage points. In smartphones – the most profitable and fastest-growing segment of the mobile phone market – Samsung has pulled ahead of Apple, shipping 28 percent of all smartphones compared to Apple’s 20 percent. The next highest entrant in smartphones, Nokia, didn’t even come close with its 5 percent.

The legal battle is old news and pretty much irrelevant in the face of Samsung’s market power, according to many analysts. The case was all about designs in Samsung’s older models, they said, and won’t have any impact on the company going forward. The monetary damages (which the judge reduced in early 2013 to $600 million) amount to pocket change for a powerful manufacturing and financial engine that is hitting on all cylinders.

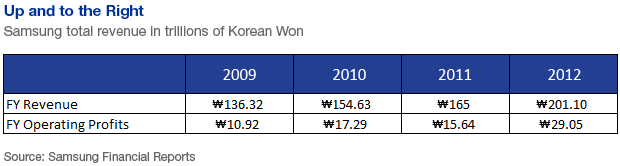

Samsung has been posting steady gains in both revenue and profit over the past few years and looks poised to continue the trend. In January, the company reported 2012 Q4 revenues of $52.4 billion, up 19 percent from Q4 2011, with operating profits of $8.3 billion, up 10 percent from Q3 2012 and up a whopping 89 percent from Q4 2011. In Q1 2013, which ended March 31, Samsung posted operating profit of $7.9 billion, more than 50 percent higher than in Q1 2012, the company announced in late April.

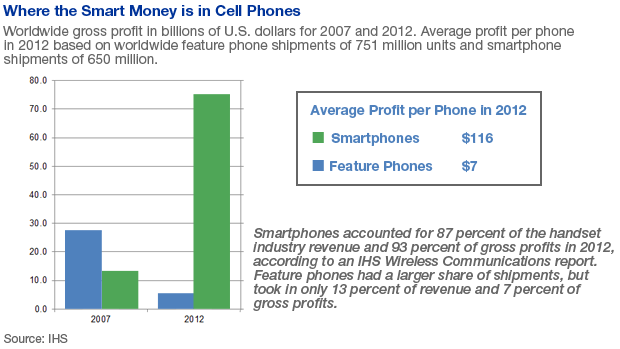

As smartphones come to dominate the mobile handset market - IHS forecasts they will make up 56 percent of the handset space in 2013 - Samsung and Apple are settling into what looks like a duopoly. Because of their dominance in the more profitable smartphone sector, the two companies together account for 81 percent of gross profits in the mobile handset industry, according IHS. As the market consolidates, so do the profits, as shown in the chart below.

It’s about the supply chain

While the general press monitors the public move of each company (such as Samsung’s U.S. marketing binge last year, in which it outspent Apple by $68 million, according to ad research and consulting firm Kantar Media), the real story is playing out behind the front lines, in the supply chain trenches. After several years of what might be called co-opetition, during which Samsung was a major component supplier to Apple as well as its biggest competitor, the two companies are going their separate ways.

Originally, Samsung and Apple jointly designed the application processor for the iPhone. Then Apple took its design in-house, designing its own application processor, but still used Samsung to manufacture it. Most recently, there are rumors that Apple will move its application processor production to TSMC.

Over the last three years, “Apple’s repositioned itself so it’s not beholden to Samsung,” said Steve Mather, senior principal analyst and subject matter expert at IHS. (Click here for a February 2013 video of IHS’ Mather discussing Samsung’s Ascent.)

But Samsung may be the better-positioned of the two companies. Because of its vertical integration on the hardware side, it’s not beholden to Apple, or anybody, say analysts. Indeed, it designs and manufactures four of the most valuable components in handsets: application processors, DRAM, NAND flash and displays – which together constitute about two-thirds of a phone’s bill of materials, according to Mather.

However, exactly how Samsung’s supply chain gives it an edge is a topic of speculation and even disagreement among analysts. Does the fact that Samsung makes its own components give it a cost advantage? Or is it more of a technology advantage? Aren’t the huge capital costs of making its own components a large and risky burden?

“It’s very much a mix. And that’s the piece I think people miss. It’s very easy to paint [Samsung’s supply chain strategy] as a simple picture,” said Doug Freedman, an analyst at RBC Capital Markets. “It’s not just a matter of being vertically integrated or potentially cutting costs by owning much of its own supply chain. It’s much more complex,” he said.

Mather agrees. Vertical integration doesn’t necessarily confer upon Samsung a magic formula for succeeding in the market. After all, Nokia used to be vertically integrated — and yet it still got clobbered in the market.

“The difference is that Samsung doesn’t do vertical integration the way most firms do it,” he said. Most large companies come to vertical integration by starting out with making an end product. Then they decide to make their own components or buy their component suppliers in order to cut costs. That means they view their component divisions as cost centers.

Samsung, however, started in the components business and then branched out into manufacturing end products such as phones, said Mather. Its components businesses started as profit centers, not cost centers, and they are still treated that way today. Each of the four component businesses dominates its market and is profitable in its own right.

Samsung makes no secret of the power of its component businesses. “If you want to see where the real action occurs, and where our industry is going, you must pull back the top layer,” Stephen Woo, president of Samsung Device Solutions, said in his keynote at the Consumer Electronics Show in January 2013. “We are creating new game-changing components across all aspects of [mobile devices].”

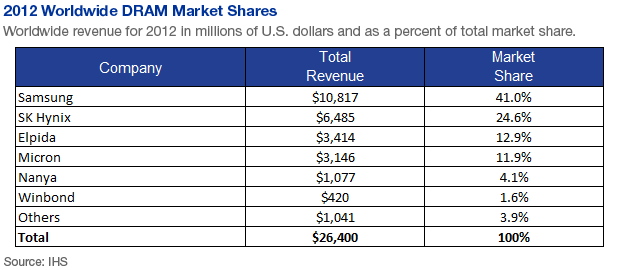

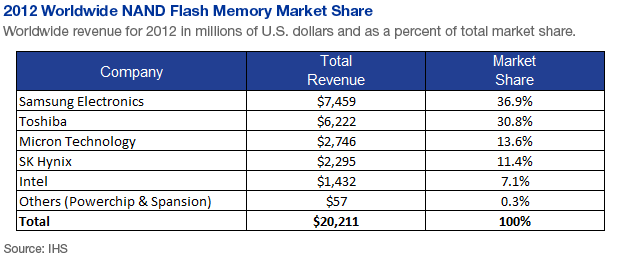

The company is the leader in the two types of memory used in mobile phones: DRAM, where it has 41 percent of the market and NAND flash, where it has 37 percent of a market that IHS expects to climb to $22 billion this year (see tables below). Samsung also manufactures application processors and the RF baseband chips that go into mobile handsets. “Right now [Samsung’s] top customers for those products, especially application processors, are Apple and Samsung itself,” said Francis Sideco, senior principal analyst of consumer electronics and communications technologies at IHS.

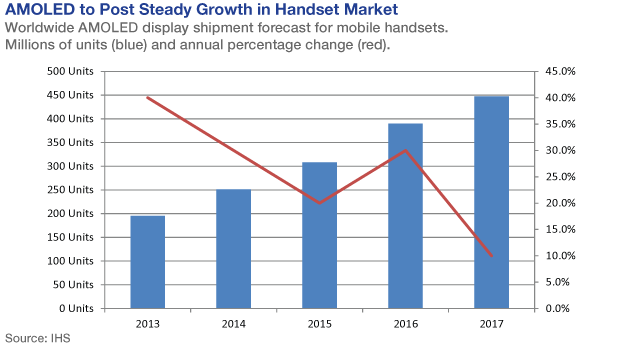

Samsung also makes displays, including LCDs. There is little profit in LCDs, however, so the company has been shifting its focus to a new technology called active-matrix organic light-emitting diode (AMOLED). AMOLED provides better color saturation and faster response times than LCDs, and is gaining market share in mobile handsets, according to Vinita Jakhanwal, director for mobile and emerging displays and technologies at IHS.

IHS forecasts that AMOLED shipments for mobile handsets will grow from 195 million units this year to 448 million units by 2017. The technology already has a 23-percent share of the smartphone market, and its share of the overall mobile handset display space is predicted to grow from 8 percent this year to more than 15 percent in 2017.

Samsung is the only company currently manufacturing OLEDs for mobile handset displays, according to Jakhanwal. Today, some 80 percent of its production goes internally to Samsung Electronics, with 17 percent going to Nokia and 3 percent to Motorola. Apple is conspicuously absent from the top tier of mobile phone makers using OLED displays.

“Apple hasn’t used OLED displays because the OLED industry is characterized by a single supplier that happens to be a company under the Samsung umbrella,” noted Jakhanwal. Samsung promotes its OLED screens in the company’s marketing, while Apple has heavily marketed its high-resolution, LCD-based retina displays, she notes. Apple is currently sourcing iPhone displays from LG Display, Japan Display Inc. and Sharp. For tablets, Apple’s LCD suppliers are LG Display, Sharp and AUO.

Source of competitive advantage

Samsung’s dominance in these strategic components gives it several advantages.

First is cost. According to Wayne Lam, senior analyst in wireless communications at IHS, Samsung’s internal transfer cost of using its own components is significantly lower than the price at which the company sells the same components to an outsider. “Operationally that means you lower your bill-of-materials cost by 10 to 15 percent,” he explains. “That’s a huge boost to your gross margins on the phone.”

But Mather isn’t so sure that there is a cost advantage — or that if it exists, it even matters. Each Samsung unit is responsible for its own P&L, he said. So why would the semiconductor division sacrifice some of its profits for the benefit of the handset division? “The point is, whether it gets an advantage or not, Samsung is making good profits,” he said.

Second is an assured supply of critical components. While DRAM and NAND are commodities, it doesn’t hurt to be the one making them if an unexpected surge in mobile phone sales constrains supplies in these historically volatile markets. And in one of the highest value-add components of smartphones and a key differentiator – the display – Samsung has a lock on the only source of supply in the market.

Third is technological innovation and differentiation. With deep knowledge of one another’s product roadmaps, the processor division can take advantage of emerging capabilities in memory design or display technology, for example. By developing its own display technology – which is the first thing consumers notice when they pick up a phone – Samsung can set its phones apart from the pack.

A case in point is Samsung’s Galaxy S4, which hit the market in April. The smartphone features the first full high-definition OLED display on the market. “Most of the phones on the market have the same features, so the display is one way to distinguish yourself,” said Jakhanwal.

But perhaps the most important advantage is the range of choice Samsung has in all these areas. Samsung does not always use its own components, or even the same third-party components, in every handset, noted RBC’s Freedman. “It’s very much a mix of sourcing internally and externally,” he said.

And the company doesn’t shy away from sourcing from the outside. In some instances, for example, Samsung has used NAND flash from SanDisk, Freedman said. In one version of the Galaxy S4, it uses Samsung Exynos 5 Octa application processors. But in another version of the S4, it uses Qualcomm’s Snapdragon 600.

“Samsung is willing to try components from anybody that can show them some sort of differentiation,” said Freedman. In contrast, Apple tends to use the same components in all its products. “You’ll find the same application processor in the iPads as Apple uses in its iPhones,” he added. Samsung may also use a carrot-and-stick approach with chip companies vying for a place in its handsets, designing in certain chips if the semiconductor company signs on with Samsung as its foundry, according to Freedman.

Indeed, Samsung uses a variety of levers to influence the market. For example, Mather contends that the company could be making more profit on its handsets. Apple’s margins are about 40 percent, while Samsung’s are 20 percent, and the rest of the pack are between 0 and 5 percent, he noted. “Samsung is exerting its control and pressuring the other handset OEMs with that margin,” he said.

Of course, Samsung’s vertical integration is not without risk. The company needs to continue to make large capital investments and keep its fabs churning out chips. And its semiconductor foundry business will take a significant hit if Apple takes its application-processor business elsewhere. According to Sideco, Apple orders made up a “significant portion of the fab’s output,” although he declined to give a specific figure. “It will hurt them on the semiconductor side, but not necessarily on the handset side,” he notes.

But Mather thinks Samsung can easily fill that excess capacity. That’s because its foundry is experienced in making application processors in one of the hottest markets around, so there will never be a shortage of customers looking for capacity. “Samsung can probably backfill the fab with more profitable business than it was getting from Apple,” says Mather.

Freedman said he heard that Qualcomm – which supplies processors for Samsung handsets models - may be lining up for it.

Mather noted that Samsung handset revenue grew 70 percent last year, and he expects the company will continue to grow its profits as well. He expects the electronics behemoth to maintain a good run with mobile phones for at least the next five years. “Samsung really has a machine that is unique in the world right now.”

SIDEBAR

The software side of vertical integration

Samsung may be playing the hardware side of vertical integration smartly, but it’s not doing as well when it comes to software, services and content.

“It’s increasingly clear that the model of a handset maker is becoming very vertical. It’s impossible to separate a smartphone device from the operating system, content and services,” said Ian Fogg, director of mobile and telecoms and head of mobile for IHS in London. “Those things are becoming increasingly integrated.”

The classic example of the right approach is from Apple, which has had great success in the vertical integration of the software, content and services with the actual end devices – the iPhone and iPad. That means a user can’t install an app without going through the App Store. “Apple has interposed itself into the value chain,” said Fogg.

Apple’s competitors, including Google, responded by adopting similar models. But Samsung doesn’t have its own operating system. As a component supplier, its strategy has been to sell handsets for all operating systems, including Symbian, Android and Windows. Android was the one that took off.

Yet Samsung is far behind in building a differentiated ecosystem on the services and content side. Although it has launched its own suite of services, including Music Hub, Video Hub and Readers Hub, “it is late to the game, and users don’t get the same benefits as they do with Apple,” said Fogg.

Apple has hundreds of millions of registered users – people with Apple IDs that are tied to a credit card, Fogg explained. Google has also corralled its users from Gmail, Google+, Google Drive and other services into one standard Google ID.

But while Samsung has nothing of that scale, it is increasingly trying to integrate software, hardware and services on its devices, said Fogg. It has its own optimized version of Android, for example, that takes advantage of new sensors and input mechanisms. In the Galaxy S4 handset, this combination increases security and connects with Samsung’s services.