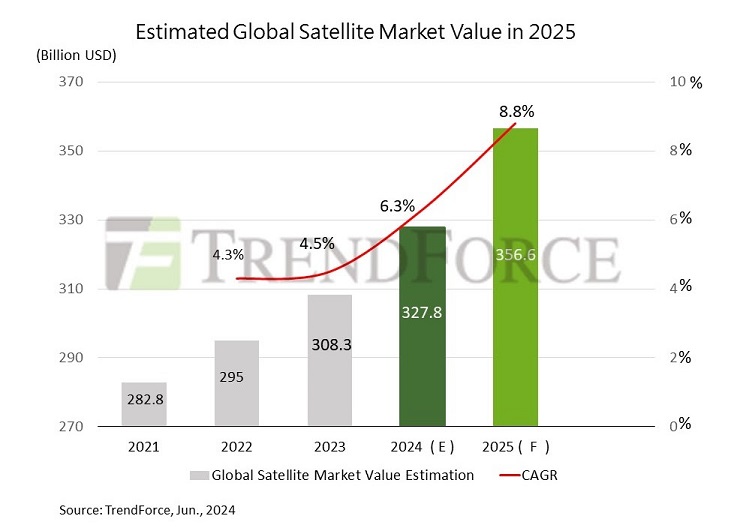

A new report from market research firm TrendForce forecasts the global satellite market value is projected to grow to $357 billion by 2025, up from $283 billion in 2021.

As rising penetration rates of low Earth orbit (LEO) satellite services grow substantially, component makers are navigating different paths to join the supply chains of leading developers Starlink and OneWeb.

Starlink employs vertical integration strategy for its supply chain while producing and assembling satellite components in its factory in Redmond, Washington. These include:

- Payload channel elements

- Ka-band antenna elements

- Filters

- Separators

Different strategies

TrendForce said because Starlink makes these components in-house the company effectively controls production conditions and reduces the complexity of supply chain management.

Juxtapose to OneWeb, which has a highly outsourced supply chain strategy where it relies on key satellite components from parts manufacturers. These components are then partially assembled by subsystem factories before being sent to OneWeb’s factory for final assembly. This model is a more open supply chain model that allows OneWeb to work with several third-party companies for entry into the LEO satellite market.

Because of these different strategies, Taiwanese LEO satellite makers are finding dissimilar paths in the supply chain.

While larger Taiwanese LEO satellite component vendors can integrate into the Starlink supply chain due to more resources and capability to meet Starlink’s space testing requirements, medium and smaller LEO suppliers cannot due to limited resources, TrendForce said.

There, TrendForce said small- and medium-sized LEO satellite component makers will need to partner with open supply chain vendors like OneWeb to enter the market.