The U.S. and European Union are accelerating plans to build new semiconductor fabrication facilities through government incentives and subsidies with the goal to create a more resilient semiconductor supply chain and bolster self-sufficiency.

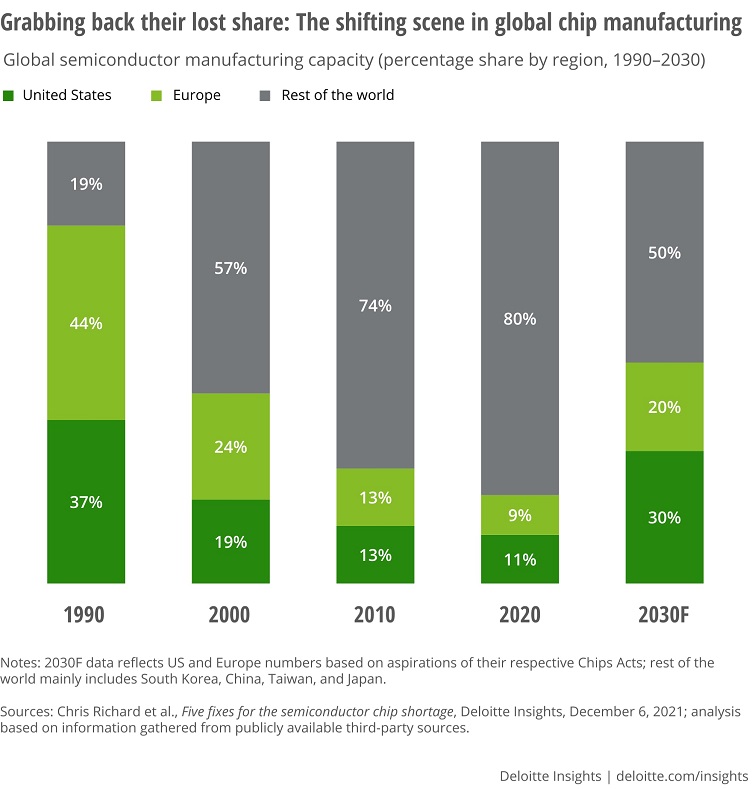

Part of the reason for these moves is due to the manufacturing footprint spread unevenly worldwide — more than 80% of semiconductor manufacturing is found in Asia, specifically Taiwan and Korea. While gaining back the market share lost over the decades is important, the COVID-19 pandemic showed how this aggregation left the supply chain extremely vulnerable.

The result was two years’ worth of semiconductor shortages, which the industry is finally beginning to get over.

Because of this, the U.S. and European governments decided to fund investment in semiconductor fabs through subsidies and incentives, something these regions have lacked doing in previous decades while Asian governments funded the growth of their semiconductor supply chain. This investment includes the $52 billion CHIPS and Science Act that was passed in August of last year and the European Chips Act, which just this month approved funding to the tune of $47 billion.

The moves are twofold: the E.U. wants to have 20% of chip manufacturing and the U.S. wants 30% by 2030; and a more regional supply chain will hopefully cushion problems if a future geopolitical issue breaks out or another crisis cripples parts of the supply chain.

Building more capacity is indeed important but it is just one part of numerous supply chain issues that need to be addressed. The following are five ways these regions can make moves in 2023 to help reshape the supply chain by 2030 and beyond, according to recent insights from market research firm Deloitte.

1. The right balance

The first step for these regions is to find the right supply chain and manufacturing balance, including how to rethink their manufacturing footprint based on evolving trade restrictions.

This includes:

- What parts of the supply chain must be domestic.

- What parts could be in geographies close to the home country.

- What parts of the supply chain should be in friendly or allied countries.

- What parts should be offshored even in potentially problematic geopolitical situations.

Deloitte said that because the global chip supply chain is so distributed that every country will likely have to rely on someone else, even if they are less friendly or unfriendly to the host region. Finding the optimal mix and how it can change over time is the challenge.

2. Moving assembly and testing closer

While many of the recent moves involve building new semiconductor fabrication plants. These expensive and big factories must eventually go to the back-end assembly and testing plants. This could open a new problem if these facilities are not close to the domestic region.

Leaving all the assembly and testing in Asia could do little to mitigate supply chain risk, Deloitte said, and the U.S. and E.U. should invest in these less glamourous facilities that are still critical to the semiconductor supply chain.

3. Forming alliances

Third, these regions should look to bolster manufacturing capabilities by fostering strategic partnerships and alliances. A consortium-based approach could help to build capabilities for the future. This could come in the form of semiconductor partnerships, government deals and even agreements with private equity firms, construction contractors and equipment makers.

4. Prioritize talent

It is one thing to build new fabs and test facilities, it is another to fill these facilities with the right workers and skilled employees to operate them.

Deloitte said the U.S. and E.U. need to attract talent from allied countries and regions with favorable immigration policies. Additionally, governments should fuel STEM education programs to help build required skills and talent among the domestic workforce for the future of the semiconductor supply chain.

5. Modernization

Finally, Deloitte said semiconductor manufacturers should take the opportunity to push the envelope in modern manufacturing to improve yields, reduce operating costs and use emerging technologies such as cloud computing and artificial intelligence.

The full research can be found in Deloitte’s 2023 Global Semiconductor Industry Outlook.