As the electronics components industry's foremost trade organization, the Electronics Components Industry Association (ECIA) has deep knowledge about the manufacturers and supply chains that deliver critical, advanced technologies around the globe. By extension, due to the global reliance and ubiquity of technology today, the electronics industry can be analogue to assessing the global economy at large.

Who better to ask about trends in chip manufacturing than Dale Ford, chief analyst for ECIA. Ford is a highly respected industry analyst with extensive experience producing award winning market research. He brings 30 years of expertise in technology trends, competitive analysis, forecasting and supply-demand research of the electronics, semiconductor and electronics components industries.

What is the most surprising thing about the semiconductor industry today to you?

My favorite word to describe the semiconductor industry today is “resilient.” The performance of the industry in the face of the daunting challenges of the past few years has surpassed all expectations.

We have all lived through the past few years and seen the broad-based impact of the pandemic and related crises on our world. In the midst of this, the semiconductor industry has generated incredible growth, both in revenues and unit shipments, and stepped up to alleviate the supply chain concerns of many distressed industries. Yes, the automotive industry took a major hit. But it could have been much worse without the responsive actions of the semiconductor industry.

Demand for semiconductors has been so strong that there was great concern that the supply of chips would be a critical bottleneck for the electronics industry. With demand rebounding in the summer of 2020, semiconductor suppliers and supporters in the supply chain have stepped up. Since the start of the recovery two years ago, worldwide unit shipments of logic ICs has increased by over 63% according to WSTS statistics. Analog IC unit shipments have jumped by over 50% and discrete semiconductor shipments have expanded by over 30%. Remember that it takes two to three years to bring a new fab online once construction has started. This amazing growth in supply was delivered without the benefit of injections of increased capital investments beyond previous plans.

After so many years following the semiconductor industry it is hard to say that I am surprised anymore after seeing its continued success. A more accurate word to describe my experience is “amazed.”

How are economic factors, such as a looming recession and labor shortages or skills gaps, affecting the electronics supply chain? What about domestic manufacturing?

The electronics and semiconductor industries have become so global and ubiquitous that a synergistic bond has been created between the industry and the overall economy.

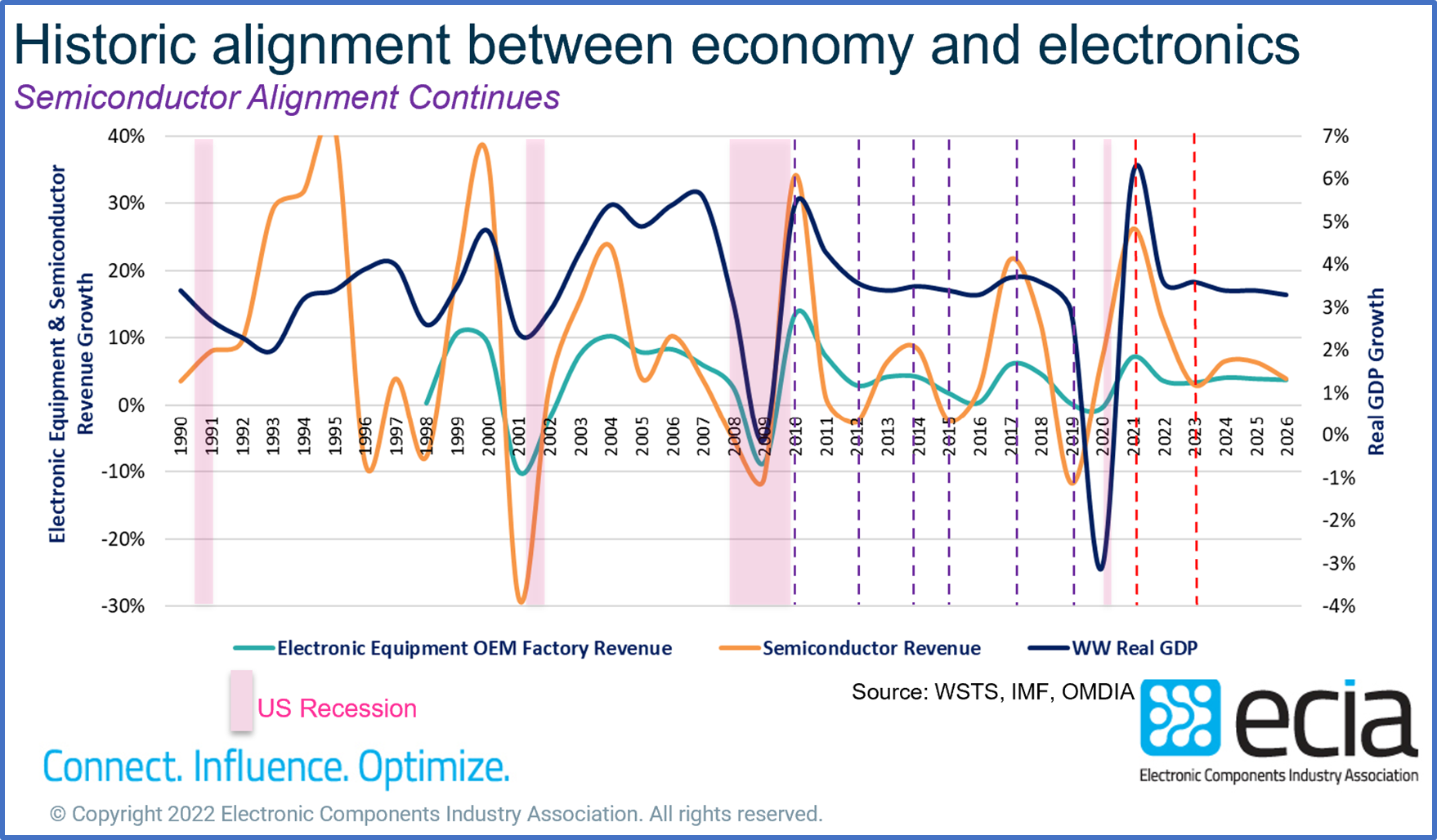

Revenue growth in the early days of electronics was driven by consumer electronics products and multiple generations of PCs. The growth in the electronics industry was fairly independent of the world around it and was mainly aligned with the introduction and adoption of exciting new products built on new, advanced technologies.

That all began to change in the second half of the 1990s. With the spread of the internet, increasingly globalized markets, and penetration of electronics into every industry and consumer segment, the electronics industry growth started to align with the overall economy. The bond grew even stronger with the spread of communication technology and reach of digital handsets, followed by smartphones.

When annualized semiconductor revenue growth is compared to GDP growth, it is seen that both have been aligned since the mid-1990s. In fact, the correlation with a period of recession is not really significant. What is most significant is if the economy, represented by GDP growth, is on the upside or downside of its cycle. I argue that the influence is not a one-way street. Electronics and technology have grown to exert such a strong influence on the economy that they are a major contributor to economic performance.

Historical alignment between economy and electronics. Source: ECIA

Historical alignment between economy and electronics. Source: ECIA

Factors such as labor shortages and skills gap are just a few of the macro-environmental factors that impact the electronics supply chain. In the past year inflation and the impact on material and labor costs have played an increasing role. Analysis similar to the GDP analysis described above also shows that when the consumer price index passes a certain threshold it signals an eventual downturn in the growth of semiconductor and electronic revenue. In the near term, increased prices may provide a temporary boost to growth, but it eventually clips the wings of growth.

I have found the Lehigh University Supply Chain Risk Index to be a helpful barometer of the pressures faced by participants in the electronic components supply chain. While this index measures overall supply chain pressures, in my experience it also accurately reflects those pressures in the electronics industry. In the report for Q2 2022, transportation disruption and economic risk clearly outpaced all other risks.

In your opinion, how can government help address supply chain issues and domestic chip manufacturing? Or is the government’s involvement counterproductive?

The topic of government involvement in supply chain issues and domestic chip manufacturing has been the source of debate. The Semiconductor Industry Association (SIA) has been a strong advocate of the CHIPS Act of 2022 that was recently passed by U.S. Congress. In the view of the SIA, this act will “strengthen domestic semiconductor manufacturing, design and research, fortify the economy and national security, and reinforce America’s chip supply chains.”

SIA points to the erosion of the U.S. share of modern semiconductor manufacturing capacity from 37% in 1990 to 12% today. The centralized location of a large share of critical semiconductor manufacturing technology in Taiwan has created a major national security issue as it is under increasing threat from China. Treasury Secretary Janet Yellin has been promoting the importance of “friendshoring” the electronics component materials and supply chains. The arguments in favor of government investments are very powerful.

On the other hand, opponents of government intervention and investment raise very legitimate concerns. Perhaps the most significant being these decisions are typically driven more by political considerations instead of business or technology. There are many painful examples of government investments in green technology companies that were complete failures and distorted the local manufacturing economy. In addition, some have argued that government investments have been misused by companies as they take the savings to invest in China and offshore manufacturing jobs. The accountability and transparency issues when government funding is involved are of great concern. Finally, government money always comes with government regulations and rules that usually add to the costs of manufacturers and supply chain participants.

The lobbying forces in Washington, D.C. are powerful and only a few major industry bodies are in a position to influence decision making. In my discussions with industry executives, I have found that most simply accept the fact that the government will choose what it wants to do, and it is up to the companies in the supply chain to adapt to whatever policies are adopted.

I believe that is the most realistic approach to government involvement in the industry.

Are supply chain problems influencing the black market for counterfeit parts? If so, how?

Following a pattern of behavior that has persisted for many years, the extremely long lead times for critical parts has created opportunities for components to be supplied through the non-authorized channel. In some cases, this simply means parts that have been recycled or sourced from areas other than channels approved by the manufacturer.

However, this opens the door for the black market and the supply of counterfeit chips. Whether innocent or not, the risks to those who purchase these parts is the same: legal liability, penalties, lost profits and more. There continue to be new technologies introduced that attempt to identify counterfeit chips. The message of ECIA is that the only true safety is by procuring components through the authorized channel. ECIA has published extensive research on the issue of counterfeiting that can be found on its website in the Issues & Practices section.

Be it 7 nm or 3 nm, the shrinking sizes of transistors is a major trend. How small can major chip manufacturers go, realistically speaking? How does this complicate lead times and supply? What technologies are over-the-horizon?

In discussions of Moore’s law, a famed quote from Mark Twain might be most appropriate. When one major American newspaper [wrongfully] printed his obituary, Twain quipped: “The reports of my death are greatly exaggerated.”

The amazing technological advances of semiconductor technology continue despite predictions that we have come to the end of the road in process geometry shrinks. The battle between TSMC, Samsung, and Intel for the lead in process geometry size continues to push the boundaries of physics.

TSMC recently announced that it is introducing 3 nm chips in the second half of 2022 and will bring 2 nm technology to the world stage in 2025. Looking ahead to 2024, Intel expects to finalize the design for its first chips with transistors smaller than 1 nm. They'll be measured by angstroms, instead. The Intel 20A node will be powered by RibbonFET transistors, the company's first new architecture since the arrival FinFET in 2011.

A common belief is that we appear to be in an era of a modified Moore’s Law, where the pace of transistor change has slowed. However, Intel's CEO Pat Gelsinger believes that Moore's Law is far from obsolete. As a goal for the next 10 years, he announced not only to uphold Moore's Law, but to outpace it. Last year, he stated, “We are leveraging our unparalleled pipeline of innovation to deliver technology advances from the transistor up to the system level. Until the periodic table is exhausted, we will be relentless in our pursuit of Moore’s Law and our path to innovate with the magic of silicon.”

The continued pursuit of transistor process geometry shrinks is part of what has been called “more Moore.” But now major advances are being categorized as “more than Moore.” These advances are pursued in the areas of system level differentiation, differentiated silicon, packaging and others. Arther C. Clark stated, “Any sufficiently advanced technology is indistinguishable from magic.” Clearly, the magic of semiconductor technology will continue!

What markets do you see having the most explosive growth over the next 5-10 years? Is it transportation? Wearables? Industry 4.0? Consumer? Something else?

In the past, specific technologies and products can be identified as the primary driver of growth in the electronics and electronics components industry, such as consumer electronics, multiple PC generations, internet and smartphones.

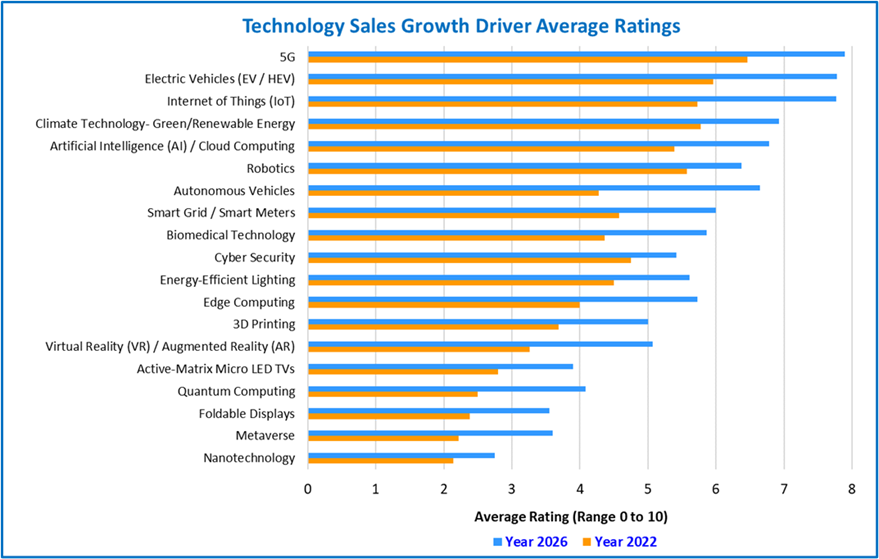

I believe the current cycle has been driven by the confluence of three major technologies and their adoption across multiple platforms – 5G, internet of things (IoT) and the Cloud. In a 2022 survey of top electronics component distribution executives, they were asked which technologies would be the most significant drivers of sales in 2022 and 2026. The results of this survey are shown below.

Source: ECIA

Source: ECIA

Ultimately, I believe it will not be a single technology or market that will drive the electronics industry. Growth will be driven by the refinement and adoption of integrated solutions that are customized around the “me point.”

I would compare these new technologies to an elite athlete whose strength is based on multiple advanced physical systems working together. In this metaphor, the data processing and storage technologies are the brain. The various senses are the image sensors, solid-state and physical sensors and human-machine interfaces. Similar parallels exist for semiconductors, batteries and more. Taken together, these technologies are optimized for a specific sport, such as basketball, swimming, soccer or gymnastics.

Eventually technologies will be advanced to the point where customized solutions will be available down to the individual level -- the me point. Achieving this will drive growth in the marvelous world of technology in the long run.

[Discover more about semiconductor technology and suppliers on GlobalSpec.com]

Is the supply stronger or weaker than it was 5 years ago? Do you see it as stronger or weaker 5 years from now? Why?

In my assessment, the supply chain is much stronger today than it was five years ago. Leaders in the industry have continually learned from experience and adopted new practices to improve performance and efficiency. Certainly, the adoption of digital technology, automation, data analytics, etc. have delivered a great boost.

ECIA engaged in many activities that have and will deliver important benefits to players in the supply chain. A partial list of recent contributions by ECIA and its members includes the launch of the Paul Andrews Continuing Education (PACE) program for training new electronics supply chain professionals, business review best practices identification, design registration studies to support greater efficiency and performance, environmental compliance updates, China tariff analysis and cybersecurity and fraud prevention best practices.

This is an industry that will continue to deliver improved performance as it works together to optimize the performance of the supply chain.