Wearable device shipments reached 444.7 million units in 2020, rising 28.4% for the full year, according to new research from International Data Corp. (IDC).

The market was driven by an uptick in hearables as they became a must-have device with new devices and lower prices becoming a trend especially as the COVID-19 pandemic continued to cause lockdowns and social distancing mandates. Hearables provided a new degree of privacy during quarantine at home or out in public.

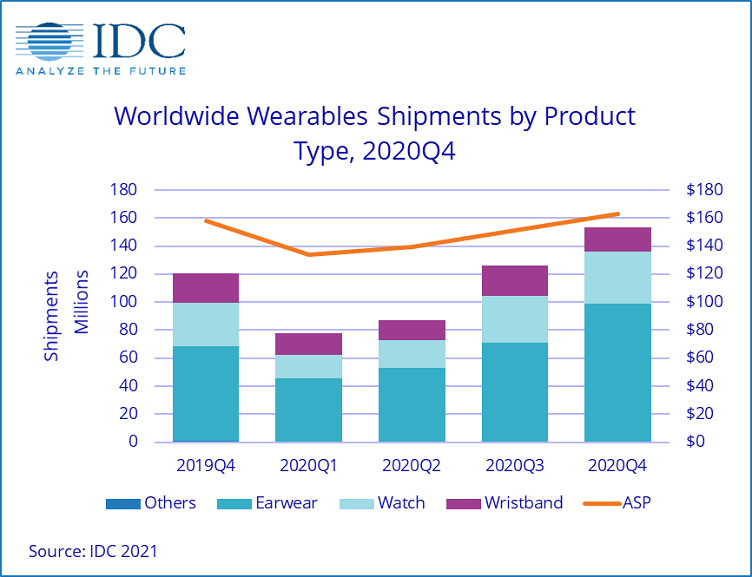

Hearables were the largest category of devices with a 64.2% share of shipments.

“Underpinning the hearables market was a constantly shifting competitive landscape, with companies slowly gaining a foothold in the market (Amazon and its Echo Buds and Frames), vendors introducing new form factors (Apple and AirPods Max), and new features making their way down the price curve, including automatic noise cancelling and voice assistant capability,” said Ramon T. Llamas, research director for IDC's Wearables Team.

While hearables surged, growth in other wearable sectors was affected by the global semiconductor shortage. Particularly, wristbands declined 17.8% during the fourth quarter and accounted for just 11.5% of all wearable devices shipped. The second largest category was smartwatches with a 24.1% share in the fourth quarter.

Market leaders

Apple Inc. led the market during the fourth quarter of 2020 with a 36.2% share with smartwatch shipment, rising 45.6% and hearables surging 22% year-over-year.

Xiaomi ended the fourth quarter in the second-place position, growing 5% year-over-year with growth driving by the expansion of its hearables line, which grew 55.5% since last year and is largely focused on the Chinese and Asia/Pacific markets. Samsung held the third position due to its hearables business as the company shipped 8.8 million units across various brands. Low-cost wristbands also saw greater traction and were able to compete with the Chinese vendors in a few markets although volume of these devices was low at 1.3 million units.

Huawei fell to fourth place and continued to struggle due to the sanctions imposed by the U.S. government. While shipments in China grew 9.4% year-over-year, shipments declined in previously strong markets such as Asia/Pacific, the Middle East, Africa and Western Europe.